US Dollar Forecast Q2 2022: Dollar Rate Hikes, Conversion and Safety Appeal

Dollar Rate Hikes: It is difficult to tell what role the Dollar will play in the global financial system heading into the second quarter of 2022. On the one hand, traditional risk assets have held back the tide of a more prolific collapse while interest rate expectations have exploded higher. Alternatively, there exists a growing din of concern that markets have over-reached in the post-Great Financial Crisis run and a necessary ‘de-risking’ has yet to occur.

What theme takes the lead is critical for tracking the course of the Greenback over the coming months. There are pressing matters that should be evaluated for USD projections like FOMC rate forecasts and growth projections. Through the scheduled and unscheduled event risk, however, traders should not forget the pressure on the benchmark currency to live up to its ‘systemic haven’ status as crises unfold worldwide and major economies (e.g., Russia and China) seek alternatives to the world’s principal currency.

DOLLAR: THE SAFE HAVEN

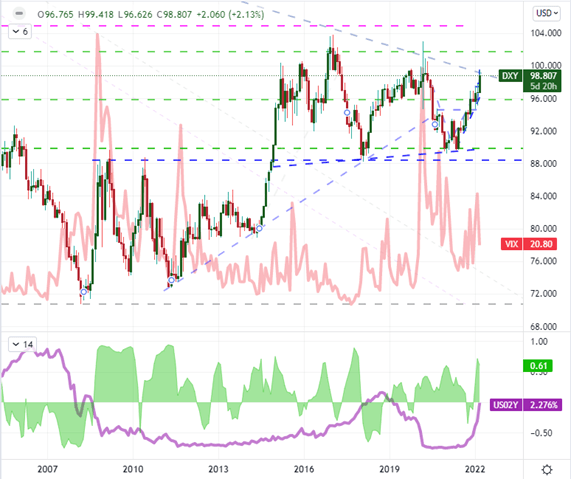

Through the opening quarter of the year, there were a few favorable fundamental winds that could have taken credit for the US currency’s appreciation. One of the more neatly correlated matters has to be the reversal in risk trends. Benchmark speculative assets like the US indices put in for a sizable retreat through much of the opening stretch of the year, and the need for safety was at times fairly intense. The scale of fear typically matters for the Greenback as more measured swoons tend to lead investors to be more discerning in where they intend to park their capital.

When US assets are sporting uncompetitive yields, that would make the currency less than ideal a vehicle in which to park your money. I still view the USD as an extreme haven when liquidity is the only consideration. Yet, with the distinctly competitive rise in the country’s benchmark rates, this may prove to be one of the more nuanced refuges. Considering how insistent Fed officials have been about their intentional push forward with accommodation withdrawal, it seems a charge will be maintained.

CHART 1: DXY INDEX OVERLAID WITH VIX, 12-WEEK CORRELATION AND US 2-YR YIELD (WEEKLY)

RATE EXPECTATIONS OUTSTRIPPING OR KEEPING PACE?

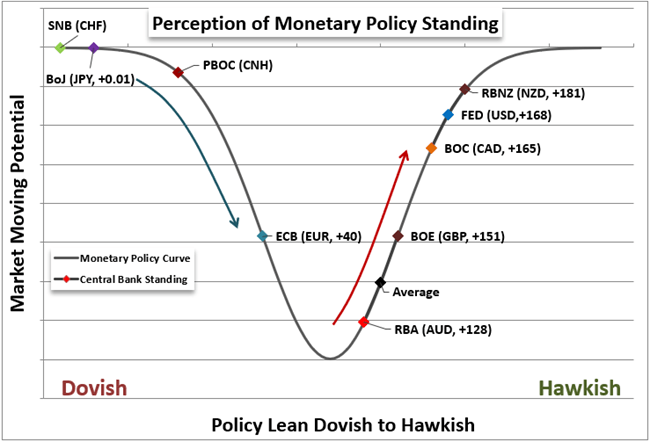

Interest rate forecasts are another critical fundamental theme to track in order to understand the Dollar’s intentions. Of course, it is essential to keep a clear sight line on the Greenback, but the relative hawkish or dovish path requires that we compare the US course to its global counterparts. Heading into the second quarter of the year, the Federal Reserve managed to feed an exceptionally aggressive forecast.

After the first-rate hike in March, the Federal Reserve upgraded its own rate forecasts from the three projected in the December SEP (Summary of Economic Projections) to a staggering 7 hikes through year’s end – all meetings with the exception of January. That put us in an unusual position where the leading and speculative market was in-line with the lagging and cautious Fed. Yet, that coincidence wouldn’t last long.

CHART 2: RELATIVE MONETARY POLICY STANCE

Dollar Rate Hikes

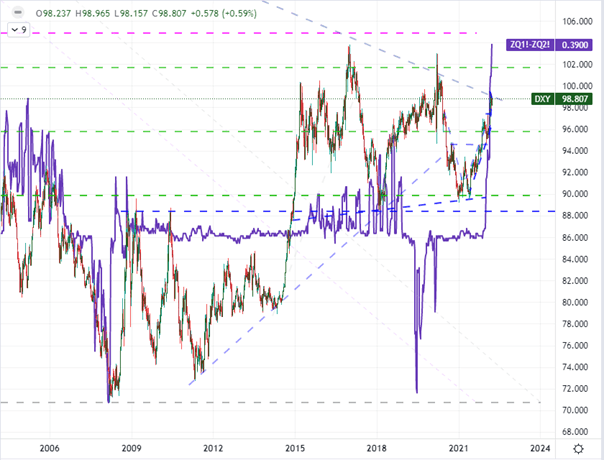

Over the coming three months, there are two scheduled monetary policy meetings and announcements: on May 4th and June 15th. At the beginning of April, Fed Fund futures and swaps were pricing in high probabilities (over 60 percent) of 50 basis point rate hikes from the group at both events. That would indeed be a very aggressive stance. It could also prove a significant booster for relative value. While the Fed is still trailing some counterparts with its primary rates of return, fast hikes can quickly close the gap – besides the markets are forward looking with analysis and pricing. For those that have come to truly believe in the ‘central bank put’, the US authority made an exceptional effort to suppress that previously warranted faith.

Why would they do that? They are trying to break a dependency. And the markets believe their warnings. Looking at Fed Funds futures, we have seen the most aggressive near-term hawkish rate forecasts in over two decades.

CHART 3: DXY DOLLAR INDEX RELATIVE TO IMPLIED FED FUNDS YIELD OF NEXT MEETING

THE OUTLIER RISK FOR THE DOLLAR: DIVERSIFICATION

Dollar Rate Hikes: In all likelihood, the Dollar will draw upon its own interest rate expectations relative to counterparts or the state of market-wide sentiment to determine the fundamental current. However, correlations can wax and wane with a shift in systemic relationships. One of the outliers matters for which I have warily watched over the past quarters and years is the effort to diversify away from the world’s most liquid currency. The push was far more broad and severe with the previous administration’s push for trade wars, but circumstances seem to cement the Dollar its previously stated purpose.

That said, there are large countries that are seriously motivated to push the world away from the USD. Russia was the more charged alternative seeker this past quarter owing to its efforts to circumvent Western sanctions. The bigger player looking to diminish the sway of the US and its currency has been China. The world’s second largest country has long harboured an interest to top the list and more meaningfully influence the global status quo. Given the unrelenting problems with Covid, trade partners’ response to Russian sanctions and overleveraged local conglomerates, there is stronger incentive to push the Yuan as a Dollar challenger. This will not be a serious threat for some time; but in the interim, it could seriously disrupt trends born out of ill-formed conviction.