US Dollar May Keep Pressuring Emerging Market Currencies Amid Ukraine and the Fed

US DOLLAR, SINGAPORE DOLLAR, THAI BAHT, INDONESIAN RUPIAH, PHILIPPINE PESO, ASEAN, FUNDAMENTAL ANALYSIS – TALKING POINTS

- US Dollar gained against most ASEAN currencies this past week

- The Federal Reserve rate decision and Ukraine remain key risks

- Indonesian Rupiah also eyeing local trade data, exports to surge

US DOLLAR ASEAN WEEKLY RECAP

US Dollar Pressuring Emerging Market: The US Dollar advanced against most of its ASEAN counterparts this past, with USD/SGD, USD/THB, USD/PHP gaining 0.14%, 2.16% and 0.71% respectively. Meanwhile, the Indonesian Rupiah was more resilient, with USD/IDR falling 0.54%. The latter could be explained by more optimistic local market conditions.

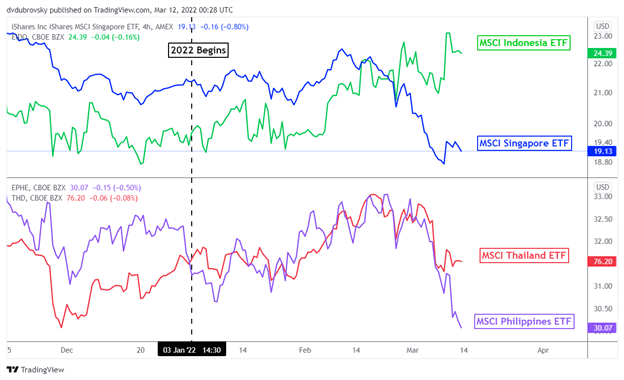

On the chart below, the MSCI Indonesia ETF clearly outperformed similar indices tracking Singapore, Thailand and the Philippines. This could be explained by Indonesia’s reliance on commodity exports as prices soar amid the ongoing crisis in Ukraine. Still, the US Dollar may remain broadly on the offensive in the week ahead.

MSCI ASEAN INDICES 4-HOUR CHART

EXTERNAL EVENT RISK – FEDERAL RESERVE, UKRAINE

The focus for emerging Asia market currencies will likely remain glued to external event risk in the week ahead. The two key risks will likely be the ongoing Russian attack on Ukraine and the Federal Reserve rate decision. Both of these events risk increasing capital outflows from developing nations, hurting their local currencies.

A Bloomberg gauge of Emerging Market capital flows dropped to its lowest since November 2020, leaving it down over 16.5% since early 2021. When risk aversion picks up in global markets, the riskiest of investments tend to be the most vulnerable to traders pulling away their capital from. Still, ASEAN economies have spent a lot of their time accumulating foreign exchange reserves since the Covid began.

US Dollar Pressuring Emerging Market

This leaves them with plenty of firepower to stem off downward pressure against their currencies if they need it. With that in mind, all eyes turn to the Fed rate decision, where the central bank is expected to begin the post-pandemic rate hike cycle. Quantitative tightening is expected to follow soon after amid persistent 40-year high inflation.

Higher interest rates increase the cost of repaying foreign debt that many Emerging Markets have accumulated over the years. This plus falling currencies increase the strain of making their repayments. A more aggressive central bank could thus amplify Emerging Market capital outflows, offering upward pressure for USD/SGD, USD/PHP, USD/THB and USD/IDR.

AESAN EVENT RISK – INDONESIAN TRADE

The ASEAN economic docket is fairly light in the week ahead. The Indonesian Rupiah will be eying local trade data. For February, Indonesian exports are expected to rise 40.47% y/y from 25.31% prior. However, imports are also anticipated to rise 42.2% y/y from 36.77% prior. All things considered, the focus for the Singapore Dollar, Thai Baht, Indonesian Rupiah and Philippine Peso will thus likely remain focused on external event risk.

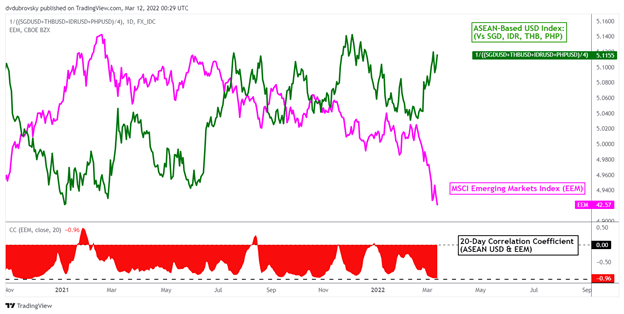

On March 11th, the 20-day rolling correlation coefficient between my ASEAN-based US Dollar index and the MSCI Emerging Markets Index changed to -0.96 from -0.94 one week ago. Values closer to -1 indicate an increasingly inverse relationship, though it is important to recognize that correlation does not imply causation.

ASEAN-BASED USD INDEX VERSUS EEM INDEX – DAILY CHART

*ASEAN-Based US Dollar Index averages USD/SGD, USD/IDR, USD/THB and USD/PHP