JPY Forecast Q2 2022: Will Inflation Surpass the Bank of Japan’s Target?

JAPANESE YEN FIRST QUARTER RECAP

JPY Forecast Q2 2022: The anti-risk Japanese Yen put in a dismal performance during the first quarter of 2022, particularly as March wrapped up. A majors-based Japanese Yen Index that averages JPY against USD, AUD, GBP and EUR fell as the S&P 500 and 10-year Treasury yield climbed.

Stocks and bond yields rising in tandem can make it difficult for the Japanese currency to shine. Russia’s attack on Ukraine and a more hawkish Federal Reserve have been unable to break market sentiment in a lasting way, at least for now. Is more pain in store for JPY ahead?

HOW HAWKISH WILL THE FED BE?

At face value, it seems more of the same could remain in store for the Yen in the second quarter. One of the leading causes of JPY weakness likely stems from increasing monetary policy divergence between the Bank of Japan and its major counterparts. Aside from the Swiss National Bank, the BOJ remains one of the most dovish G10 central banks.

Global government bond yields continued their ascent in the first quarter. Looking at Treasury rates, the 2-year surged from 0.75% to above 2.15%. The 10-year started around 1.53% and closed in on 2.4% as March was wrapping up. A more hawkish Fed was a key culprit, with policymakers leaving the door open to hiking rates in 50bps increments to bring price growth to heel. The odds of such a move by May has jumped to a commanding 75% towards the end of March.

JAPANESE YEN FUNDAMENTAL DRIVERS

WILL JAPANESE CPI SURPASS 2% IN THE SECOND QUARTER?

Central banks have been responding to rising global inflation, which seems to be occurring almost everywhere except for Japan. In February, Japan’s headline CPI rate was 0.9% y/y compared to 7.9% y/y in the United States. In response, the BOJ has done virtually nothing to adjust monetary policy. The target policy balance rate has remained at -0.10%, alongside a 0% “yield curve control” (YCC) cap on the 10-year JGB bond yield. Will this change?

Japan is an importer of key commodities like crude petroleum and coal briquettes. Russia’s attack on Ukraine has sent the prices of these key inputs soaring as the developed world looked increasingly to other sources. In fact, since Japan is a key energy importer, rising prices may have played a role in the Yen’s depreciation.

JPY Forecast Q2 2022

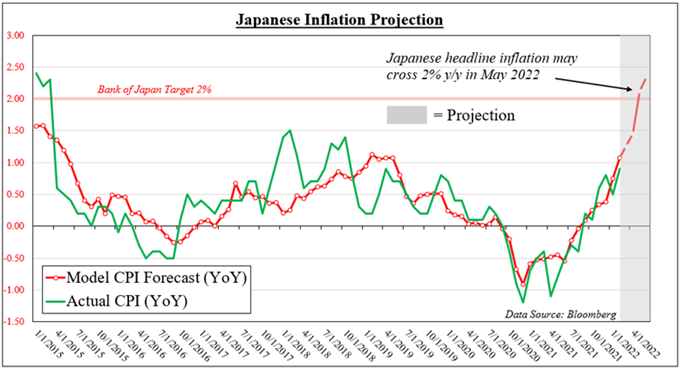

On the chart below, I have estimated where Japan’s headline CPI (YoY) rate could go from here. This is based on a multiple linear regression model that measures the impact of crude oil and coal futures on the country’s inflation since 2015. Since CPI tends to lag prices, I’ve delayed the latter by 8 months relative to CPI. This means we can use recent oil and coal prices to project inflation in the period ahead.

According to the model, Japan’s headline inflation rate may reach above 2% y/y in May. Is the central bank likely to adjust policy when that happens? Probably not. The BOJ may wait until there is evidence of persistently strong CPI data before changing tack. Moreover, the central bank has remained dormant when inflation briefly passed above its target before. Absent a market meltdown, the road ahead for the Yen is likely to remain difficult.