NZD/USD Unfazed by Trade Data as APAC Markets Eye China Lending Rate

NEW ZEALAND DOLLAR, NZD/USD, TRADE BALANCE, CHINA, PBOC, RISK TRENDS – TALKING POINTS

- Kiwi Dollar unfazed after New Zealand reports smaller trade deficit for February

- APAC traders eye possible move by China’s central bank to ease lending rates

- NZD/USD prices steady this morning as bulls eye the nearby 200-day SMA

MONDAY’S ASIA-PACIFIC FORECAST

NZD/USD Trade Data: Asia-Pacific traders have a light economic docket this week. That may leave prevailing risk-on trends

intact. Asian and US equity markets are coming off strong performances. Hong Kong’s Hang Seng

Index (HSI) gained more than 4% last week despite falling on Friday. The US benchmark S&P 500 index

rose an impressive 6.16%, the best weekly performance since 2020. The DXY US Dollar index shed

nearly 1%, even as short-term Treasury yields climbed. Euro strength was a large driver of that

weakness.

That risk-on tone helped propel the Australian and New Zealand Dollar higher versus the safe-haven

USD. Those currencies have been underpinned by the rise in commodity prices amid Russia’s invasion

of Ukraine. Other commodity-exporting countries’ currencies have also benefited since the start of the

war, including the Brazilian Real. Brazil’s central bank hiked its benchmark rate by 100 bps last week.

Despite the recent pullback in oil prices, WTI and Brent crude remain near multi-year highs, which

should continue to underpin currencies from commodity-exporting countries, especially oil exporters.

NZD/USD Trade Data: New Zealand reported trade data for February this morning. The island nation’s trade deficit crossed

the wires at NZ$-385 million, down from NZ$-1.1 billion in January. A pickup in exports helped to shrink

the shortfall. Later today, credit card spending for February and Westpac consumer confidence for the

first quarter will cross the wires, which may spur some movement in the Kiwi Dollar. It rose over 1.5%

last week, despite fourth-quarter GDP growth missing estimates.

China may deliver a cut to its loan prime rate (LPR) as soon as today. The People’s Bank of China

(PBOC) is expected to cut the benchmark lending rate by 5 to 10 basis points (bps). The move may

boost market sentiment, although there is a small chance that the rate is held steady after last week’s

surprise hold on the medium-term lending facility rate. Outside the APAC region, traders will be

watching inflation data out of the United Kingdom as well as “Fedspeak”: comments from Chair Powell

and Atlanta Fed Raphael Bostic are due. These headlines may spur movement in the British Pound and

the US Dollar.

**Click here to see what else is in store for global markets this week**

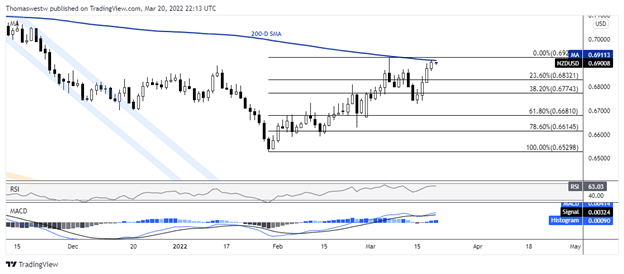

NZD/USD TECHNICAL FORECAST

NZD/USD is nearly unchanged this morning, with prices directly below the high-profile 200-day Simple

Moving Average (SMA). A break above the key SMA would put prices up against the 2022 high set

earlier this month at 0.6925. The 0.7000 psychological level would shift into focus if bulls managed to

overtake those levels. Alternatively, a move lower could see bears drive the currency pair down to the

23.6% or 38.2% Fibonacci retracement levels or the 0.6800 mark.

NZD/USD DAILY CHART