USD/JPY Resumes the Uptrend as USD Fundamentals Turn Quite Bullish

USDUUSD/JPY Resumes, turned bullish at the beginning of 2021, when it was trading at around 102.500, and it climbed to 116.30s, as the US economy accelerated and inflation started surging in the US. The FED has turned hawkish, starting to wind down the QE programme by $15 billion a month and yesterday’s press conference from Jerome Powell indicated a very hawkish FED in 2022, with many rate hikes.

This turned the USD bullish yesterday, after it had been retreating lower, and the USD/JPY resumed the bullish trend. Today, the flash reading for the US GDP report for Q4 of 2021 showed another decent increase, beating expectations as well, which is keeping this pair bullish, so we are planning to open a buy signal here.

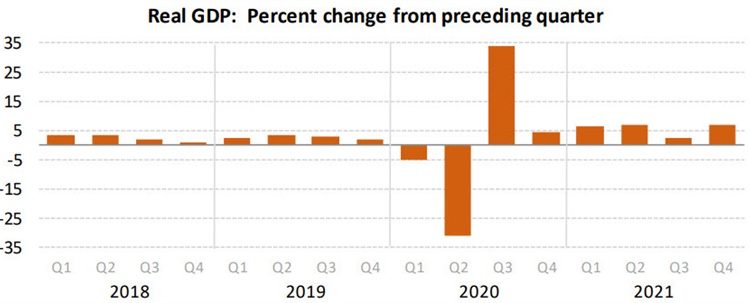

US Q4 2021 Advance GDP Repor

- US Q4 advance GDP +6.9% vs +5.5% expected

- Q3 was 2.3% annualized

- Personal consumption +3.3% vs +2.0% in Q3

- GDP deflator +7.0% vs +5.9% prior

- Core PCE +4.9% vs +4.6% prior

- GDP final sales +1.9% vs +0.1% in Q3

- Nominal GDP up 14.3% annualized in Q4

- Real GDP up 5.7% in 2021 and nominal GDP rose 10.0%

Details:

- Inventories added 4.9 pp to GDP

- Exports added 2.43 pp to GDP

- Imports cut 2.43 pp from GDP

- Home investment cut 0.03 pp from GDP

- Personal consumption added 2.25 pp GDP

- Gross private domestic investment added 5.15 pp

- Government spending cut 0.51 pp from GDP

- Full report

USD/JPY Resumes

USD/JPY Resumes, This is a strong reading, and the annual growth in 2021 was the strongest since 1984. The nominal readings are simply astonishing. A good chunk of this quarter’s jump comes from inventories, but that’s going to be a tailwind all year long, as companies move from just-in-time delivery to just-in-case inventories.

- Quite a bit of room to raise rates without hurting jobs

- Powell doesn’t rule out hiking rates at every meeting

- Improvement in labor market has been widespread and ‘remarkable’

- Labor market conditions are consistent with maximum employment

- There is a ‘very broad agreement’ on FOMC that it will soon be time to raise rates

not Fed funds

- Fed funds rate is primary means of adjusting policy (not Fed funds)

- It’s not possible to predict, with much confidence, the path of policy

- Says he doesn’t rule out raising rates at every meeting

- My strong sense is we can move rates up without undermining employment

- “Quite a bit of room to raise rates without hurting jobs. “

- We are of the mind to hike in March

- We may move sooner and faster on the balance sheet than before

- We will discuss the balance sheet at the next two meetings

- Inflation risks are still to the upside, in my view

- Inflation situation is ‘slightly worse’ than in December

- Says he’d would be inclined to raise his core PCE forecast ‘by a few tenths’

- We haven’t made any decisions on the increments of hikes

- I expect progress to be made in the second half of the year on supply chains

USD/JPY Resumes, I wouldn’t call the growth in jobs ‘remarkable’. The average for the past four months was 368K, and it was 199k last month. Meanwhile, he is not reeling in the hawkish talk at all. USD/JPY Resumes, I would have thought Powell would be more delicate with the hawkish talk, given the backdrop. Stocks aren’t going to like this.