Weekly Fundamental US Dollar Forecast: From Russia with Love; Rates Turn

- Weekly Fundamental US Dollar, But for the Russia-Ukraine conflict, the US Dollar’s fundamental moorings appear to be less supportive.

- The 2s5s10s butterfly has receded to its narrowest spread since October 2021, a sign that the US Treasury yield curve has become less supportive of the US Dollar.

- According to the IG Client Sentiment Index, the US Dollar has a mixed bias heading into the last week of February.

RECOMMENDED BY CHRISTOPHER VECCHIO, CFAGet Your Free USD ForecastGet My Guide

US DOLLAR WEEK IN REVIEW

Weekly Fundamental US Dollar, The US Dollar had a mixed week, with the DXY Index rising by +0.07%. But several USD-pairs proved more volatile than the net-change of the DXY Index, as Russia-Ukraine headlines provoked meaningful swings. EUR/USD rates settled down -0.23%, GBP/USD rates added +0.24%, and USD/JPY rates fell by -0.37%.

As US Treasury yields pullback and evolve in a manner that is less supportive of the US Dollar; the Russia-Ukraine crisis appears poised to remain the primary driver. Escalating headlines could weigh significantly on the Euro, which is the largest component of the DXY Index at 57.6%. Put simply, negative developments in Eastern Europe are good for the US Dollar right now, particularly as rates turn in a manner that have made the US Dollar less appealing.

US ECONOMIC CALENDAR IN FOCUS

The last full week of February presents a thinner economic calendar than what has been experienced over the course of the month. While there are a handful of speeches from Federal Reserve policymakers and ‘high’ rated data releases, it seems highly likely that news flow around the Russia-Ukraine conflict will; be the primary driver.

- Weekly Fundamental US Dollar, On Monday, February 21, Fed Governor Michelle Bowman will give a speech at the American Bankers Association Conference for Community Bankers.

- On Tuesday, February 22, the December US house price index will be released ahead of the US cash equity open. Shortly after stocks start trading, the February US Markit manufacturing PMI and the February US Conference Board consumer confidence reading are due.

- On Wednesday, February 23, weekly US MBA mortgage applications figures will be released.

- On Thursday, February 24, the second; estimate of the 4Q’21 US GDP report, the January US Chicago Fed national activity index, and weekly US jobless claims data will be released at 13:30 GMT. January US new home sales are due shortly after the US cash equity open. Atlanta Fed President Raphael Bostic and Cleveland Fed President Loretta Mester will give remarks at 16:10 GMT and 17 GMT, respectively.

- On Friday, February 25, the Fed’s preferred gauges of inflation, the January US PCE and core PCE reports, will be released at 13:30 GMT, as will the January US durable goods orders report and the January US personal income and spending figures are due. At 15 GMT, the January US pending home sales report will be released.

RECOMMENDED BY CHRISTOPHER VECCHIO, CFATrading Forex News: The StrategyGet My Guide

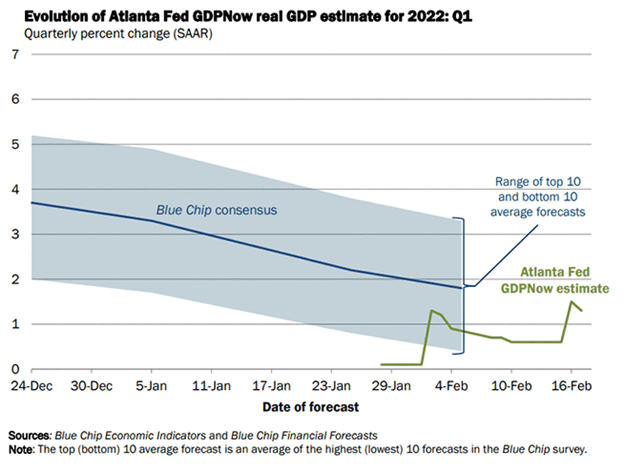

ATLANTA FED GDPNOW 1Q’22 GROWTH ESTIMATE (FEBRUARY 17, 2021) (CHART 1)

Based on the data received thus far about 1Q’22, the Atlanta Fed GDPNow; growth forecast is now at +1.3% annualized; down from +1.5% on February 16. The downgrade was a result of; “the nowcast of first-quarter real residential investment growth decreased from +4.7% to +0.3%.”

The next update to the 1Q’22 Atlanta Fed GDPNow growth forecast; is due on Friday; February 25 after the January US personal income; and spending data.

For full US economic data forecasts, view the DailyFX economic calendar.

RATE HIKES ARE COMING, THAT’S CERTAIN

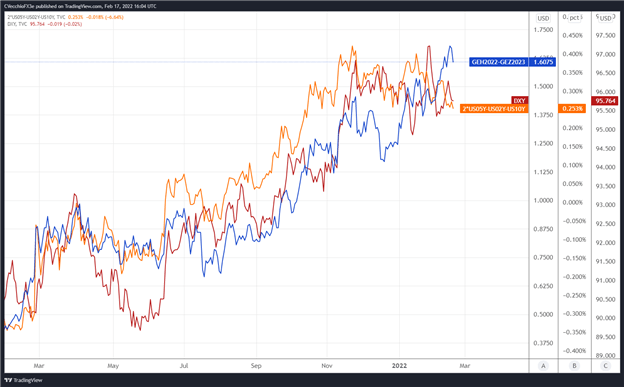

Weekly Fundamental US Dollar, Expectations for a March rate hike have crystallized. We can measure whether a Fed; rate hike is being priced-in using Eurodollar contracts by; examining the difference; in borrowing costs for; commercial banks over a specific time horizon in the future. Chart 2 below showcases the difference in borrowing costs – the spread – for the March 2022 and December 2023 contracts; in order to gauge where interest rates are headed by December 2023.

EURODOLLAR FUTURES CONTRACT SPREAD (MARCH 2022-DECEMBER 2023) [BLUE], US 2S5S10S BUTTERFLY [ORANGE], DXY INDEX [RED]: DAILY TIMEFRAME (FEBRUARY 2021 TO FEBRUARY 2022) (CHART 2)

By comparing Fed rate hike odds with the US Treasury 2s5s10s butterfly; we can gauge whether or not the bond market is acting in a manner consistent; with what occurred in 2013/2014 when the Fed; signaled its intention to taper its QE program. The 2s5s10s butterfly measures non-parallel shifts in the US yield curve, and if history is accurate, this means that intermediate rates should rise faster than short-end or long-end rates.

There are 160.75-bps of rate hikes discounted; through the end of 2023. Prior to the expiration of the February 2022 Eurodollar contract, there were 185-bps discounted through the end of 2023; in other words; a 25-bps rate hike is fully priced in for March. Rates markets are pricing in a 100% chance; of seven 25-bps rate hikes and a 40% chance of eight 25-bps rate hikes through the end of next year. However; the 2s5s10s butterfly has receded to its narrowest spread since October 2021; a sign that the US Treasury yield curve has become; less supportive of the US Dollar.

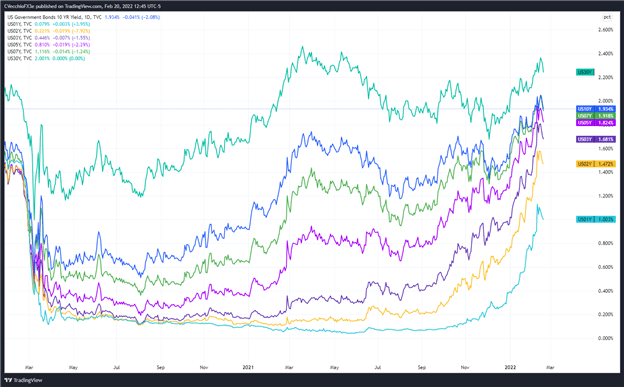

Weekly Fundamental US Dollar, US TREASURY YIELD CURVE (1-YEAR TO 30-YEARS) (FEBRUARY 2020 TO FEBRUARY 2022) (CHART 3)

The narrowing of the 2s5s10s butterfly coupled with declining US Treasury yields poses a problem for the US Dollar. If the FOMC makes clear that it will not hike rates by 50-bps in March; or suggests that inflation pressures are due to subside further – implicitly suggesting that aggressive tightening; isn’t warranted – then the US Dollar; remains vulnerable to a drop.

Weekly Fundamental US Dollar, CFTC COT US DOLLAR FUTURES POSITIONING (FEBRUARY 2020 TO FEBRUARY 2022) (CHART 4)

Weekly Fundamental US Dollar, Finally, looking at positioning, according to the CFTC’s COT; for the week ended February 15; speculators increased their net-long US Dollar positions to 35,335 contracts; from 33,725 contracts. Net-long US Dollar positioning has been holding steady for the nearly the past five months; and ultimately remains near its highest level since October 2019. The oversaturated net-long position in the futures market remains a headwind; for significant US Dollar; upside.